- The Island Investor

- Posts

- Don't Make The Same Stupid Mistakes I Did

Don't Make The Same Stupid Mistakes I Did

'Cheap' or 'Cheap for a Reason'?

Michael O'Connor

April 03, 2024

A little bit Investing, A little bit personal

👋 Hey!

Thanks for reading

I'm always happy to chat all things investing so send me your thoughts [email protected]

Everyone Loves a Sale

We all love to go shopping for a deal. If something is on sale, you can manufacture some sort of logic to justify your purchase.

Investing is no different. We're all looking for a good deal.

When I first started investing, my strategy was, "This stock has underperformed for a long time, and therefore, it will start to outperform soon.'

The strategy went something like this -

Look for companies that have gotten killed

Buy in once you see higher lows

Watch the money rolls in as the stock returns to its previous high.

IT DID NOT WORK!!!

Just because something is down 30% doesn't mean it can't fall another 30+%. Momentum is a powerful thing.

But Mike, you were surely doing fundamental research to figure out why the stock was plummeting, right?

Nope… not really. I was 22; fundamental research wasn't really 'my jam.' I had more of a 'close your eyes and hope for the best' approach at the time.

I was just screening for stocks that were plummeting, doing a quick bit of research to see if I could spot any glaring justifiable reason for the sell-off and If I couldn't find anything, I bought it.

In particular, my appetite for energy companies like Apache and Devon, at the exact time you shouldn't be buying up energy companies, was insatiable.

They say experience is the best teacher, and I have always had a 'learn by doing' approach, but this is one I wish I had learned from someone else instead of learning firsthand and stripping my trading account in the process.

So here are some takeaways to help you avoid the same mistakes.

Assuming that a stock will 'mean revert' because it used to be higher in the past is possibly the most shallow investment thesis you can have.

'It's Cheap' isn't a strong enough reason to buy something. You need to dive deeper to find that catalyst that will drive this reversal of fortunes. Without a clear catalyst, it's going to stay cheap.

Be aware of secular trends. If you are pumping your money into sectors that are part of a negative secular trend, it doesn't matter how cheap they are; they're about to get a whole lot cheaper.

Don't be an idiot like me; do some proper research. Know what you own and why you own it.

All Time Highs

This sentiment becomes even more important as we sit at all time highs.

As people see higher and higher prices for stocks, they anchor towards the price they ‘should have’ bought at. If you were going to buy Amazon at $85 last year, your default position is that you have missed your opportunity and you couldn’t possibly buy at $185 today.

Instead, people gravitate towards asset classes that are uncharacteristically cheap on a relative basis.

I think it’s a comfort thing. People who may have missed the run-up in the broader market feel it’s too late to join the game now and, instead, frantically search for the next ‘deal’ on the table.

I see the logic, but from an investment standpoint, that’s just not how it works.

Let’s take small caps stocks as an example. They fit nicely into the ‘have underperformed for a long time, and therefore will start to outperform soon’ category

And don’t get my wrong, I see the attraction. I'm looking for a deal just as much as the next guy and they are super cheap on a relative basis.

The Bull Case for Small Caps

Between 2002 and 2011, US small caps generally outperformed large caps over any 1-year period by an average of 5.1%.

Since 2012, the Russell 2000’s (small cap index) fortunes have changed relative to the S&P 500, underperforming by an average of 2.3% a year.

This reached fever pitch levels over the last year, with the Russell 2000 underperforming the S&P 500 by over 12%.

In theory, small caps should outperform large caps over a long-ish timeframe. After all, they are riskier and should generate better returns over time as a result.

Given the higher level of risk, the sheer level of recent underperformance and the current ‘cheap’ price tag relative to many large-cap names, small caps are set to outperform.

If only it were that simple.

My Take:

The 'It's Cheap' narrative isn’t a strong enough standalone reason to buy.

I've looked for that catalyst; I just haven't found it…YET

For me, the Russell 2000 is cheap, but it’s cheap for a reason.

5 reasons to be exact.

1. Higher Interest Rates

Higher interest rates are an issue for every public company, but more so for smaller ones. Their cost of capital is naturally higher, and the higher-for-longer narrative will only make this worse. Yes, some rate cuts are expected in the second half of the year, but this will still leave rates high relative to recent history.

Also, credit spreads are incredibly narrow at the moment. If spreads start to widen out, any rate cut benefits could be offset for many small-cap names.

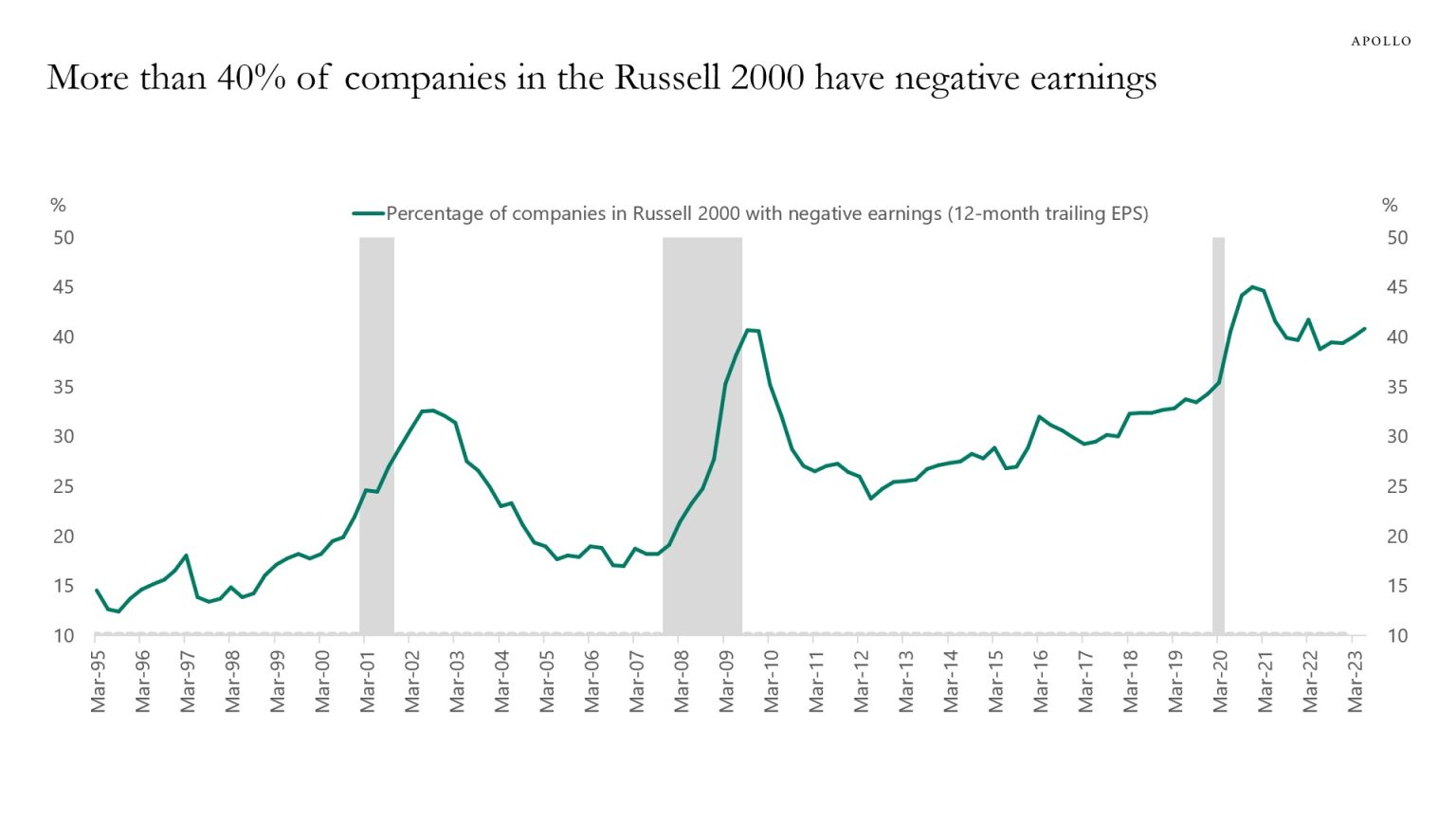

2. Negative Earnings

The rising number of small-cap companies with negative earnings doesn't help either. In a high-interest rate environment, many companies' runway to success is shortened.

You could play in the ‘S&P 600’ if you wanted to reduce the exposure to negative earnings companies here, but either way - Not ideal in a market that is primarily focused on rewarding stable, cash flow-generating companies.

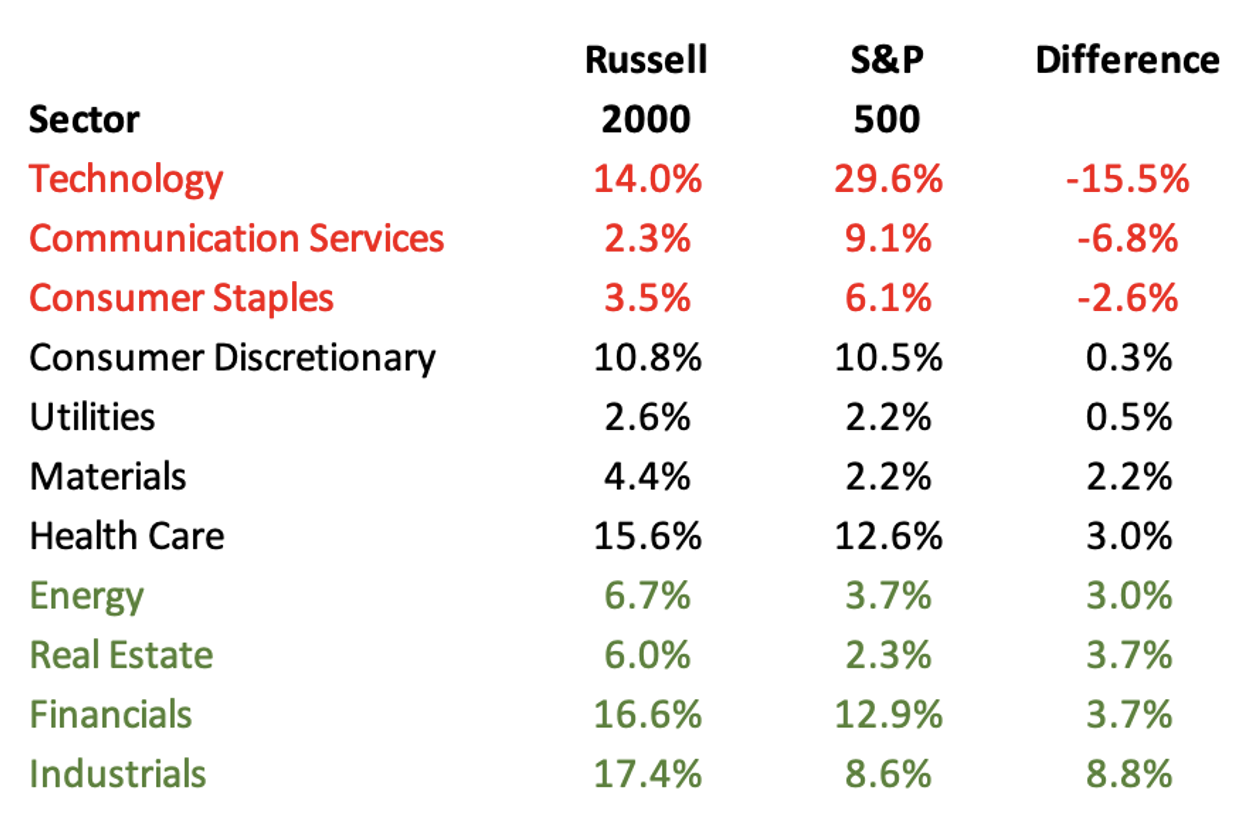

3. Sector Exposure

It’s easy to look at the sector allocation differences between the Russell 2000 and the S&P 500 and see where recent underperformance may have come from, but there is more to it than that.

Yes, the Russell 2000 has been underweight the best performing sectors. However, the makeup of these sectors is also very different.

For instance, small-cap Tech looks nothing like large-cap Tech. When we talk about the 'Tech Rally,' we are really just referring to a select number of mega-cap names with ludicrous earnings and phenomenal network effects that have seen massive gains in recent years.

If you're a 'pre-earnings' small-cap tech name, you haven't seen a penny of this 'rally.' And I don't see this changing any time soon.

Small-cap Financials look nothing like large-cap financials—if you're going to play financials, you want to play the 'too-big-to-fail' names or across the large insurance names. The small-cap financial sector is made up of 60% regional banks and real estate investment trusts. Yes, you could get a bounce off the lows here, but in my view, this isn't where you want to be in the midst of a commercial real estate crash, not to mention the regional bank crisis looming as the FED increases QT and removes the Reverse Repo facility.

What you're left with is an index that is overweight cyclicals and tilted towards the worst performing parts of their respective sectors. Remember, cheap things can get even cheaper.

4. Structural Issues

This is a less technical take, but it has always frustrated me about any small-cap index.

I don’t want to be in an index where anything that is truly excellent is getting promoted out of the index and into the big leagues (out of Russell 2000 and into Russell 1000, for example)

Every year, your best-performing names graduate. Individual stocks perform SO well, they have to be removed from the index as they have grown too large. And you have to start all over again.

We saw this happen recently with Super Micro Computers (SMCI).

SMCI provided over 100% of the returns to the Russell 2000 this year (going from $300 to $1000 in under three months will do that). Now, its new hefty valuation ensures it will be removed from the Russell 2000 and moved into the Russell 1000 when rebalancing occurs in May.

It's Index rotation for all the wrong reasons. I want to hold my winners, but hey, that’s just me.

5. Private Markets

The growth in private markets and private market exchanges in recent years has created this quasi- 'Public/Private' market that allows the best-in-class companies to remain private for longer and bypass the public small cap space.

When you have huge flows of capital allowing multi-billion dollar companies to remain private for longer, the small-cap sector losses out on some of the best performing names that would have historically grown their business within the public market.

I expect this structural trend to persist over time, resulting in many of the ‘would-be’ small-cap gains flowing through private markets instead.

Final thoughts

Small-caps have historically performed very well at the start of an economic cycle. Once the market has been washed out and interest rates have fallen, the pro-cyclical stance has tended to outperform as the economy picks up. So, if you expect significant rate cuts and a market correction, then small-cap exposure is a trade you should be lining up. I just don’t see it yet.

For me, small-cap exposure has always made more sense as a tactical trade as opposed to a long-term buy-and-hold portfolio position.

Finally, it’s just too nuanced a market to take broad passive exposure. In my opinion, if you are going to play small caps, I suggest focusing on niche concentrated active exposure or, at the very least, taking select sector exposure across the likes of Energy (PSCE) and Industrials (PSCI).

Perhaps there is a nice short term trade in there if the bounce off the November lows continue. But from a long term buy-and-hold perspective, it’s just not for me. The opportunity cost is just too high.

But each to their own.

Hope you enjoyed. 😊

I’ll be back next week with a personal story about how a small loan of a million dollars from my father changed my life…… 🧐

SHARE WITH A FRIEND❤️

Thanks for reading. If you enjoyed my newsletter, please share it with a friend.

If you didn't enjoy it - share it with 2 friends.